On 21 February 2020, the government launched a consultation on expanding the dormant assets scheme.

Having considered initial recommendations from our industry, the government is now inviting your input.

But what are the key issues that could impact UK companies with listed securities like yours? Read on to find out.

Key issue 1: Definition of dormancy

The consultation has recognised that because of the variety of the assets they are looking to introduce into an expanded scheme, the definitions of dormancy for these will need to be varied. The sectors they are looking at are:

- Insurance and pensions

- Investment and wealth management

- Securities

The securities sector definition of dormancy included in the Industry Champion's recommendations published last year has been amended:

| Industry Champion's definition |

Consultation definition |

|---|---|

|

A period of no shareholder-initiated contact for 12 years and:

|

No transactions have been carried out or contact made in relation to the asset by or on the instructions of the asset owner for 12 years and:

|

What could it mean?

The new definition could offer less flexibility by not clearly recognising the concept of a gone-away shareholder as a trigger for dormancy. The prospect of having to determine whether a shareholder has carried out a transaction or made contact with the issuer (or their registrar) is potentially complex. Hopefully, there will be some degree of flexibility to define what is reasonable in meeting this aspect of the definition. There is more information on this in our whitepaper.

There is also no solid definition of what the government would consider is needed to meet 'a legal requirement to carry out proportionate and reasonable tracing'.

Key issue 2: Full restitution

The proposals seek to define what would happen if a former securities holder whose assets have been declared dormant and transferred to the Reclaim Fund subsequently makes contact and initiates a reclaim. The consultation invites feedback on the level of restitution that the former holder would be entitled to. In 2019, the industry champion recommended that full restitution should be defined as providing:

…the full value of the shares at the point of reclaim, plus the dividends paid by the company on its shares, and, in certain circumstances, the value of any corporate actions between the point of sale of the shares and the reclaim…

This was to encourage companies to join the scheme, enhance customer protection and align participating organisations.

However, the latest consultation defines full restitution as:

…the amount that would have been due to the asset owner - had a transfer into the scheme not occurred.

The consultation wants to follow existing industry procedures. For the securities sector, this means falling back on share forfeiture practices - which are diverse, depending on the individual company.

What could it mean?

The industry champion's blueprint defined full restitution as the full value of the shares at the point of reclaim, including (if applicable) any increase in share value plus the dividends that would have been paid by the company on those shares.

The consultation has taken a different approach, which is to allow companies to follow existing industry practices and fall back on forfeiture provisions within a company's articles.

The government want the market to lead the way and expect the Reclaim Fund to reflect the practices of any company that participates within the expanded scheme. However, this could result in investors receiving different treatment from any issuers who choose to participate.

The reason for this is most company's articles don't cover the concept of restitution following forfeiture. Based on the current market practice, every company considers restitution differently. Some fix the value of the assets at the point of forfeiture, whereas others may factor in increases in asset value.

What is certain, is that few would provide restitution for distributions that have been made since the forfeiture occurred.

Could this change impact issuers joining the expanded scheme?

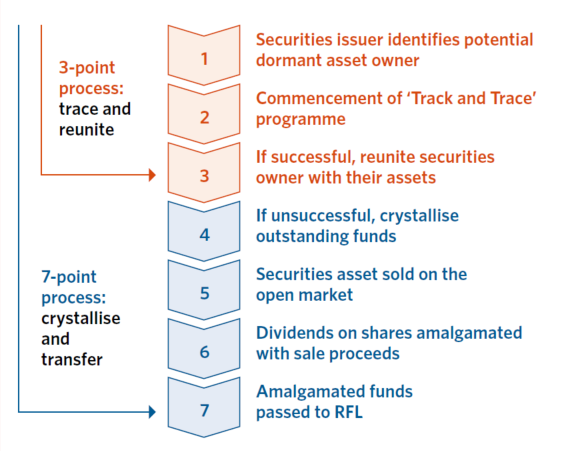

Key issue 3: Tracing and reunification

In order to participate in the expanded scheme, verification and reunification are still essential.

Therefore, the government is considering two new legislative requirements:

- Requiring participants to make proportionate and reasonable efforts, based on best practice within their sector.

- Strengthening the Reclaim Fund's ability to decline transfers where they don't feel proportionate and reasonable efforts have been carried out.

What could it mean?

The seven-stage process (below) provides a basic framework for how tracing and verification could be applied within the securities sector. Each individual company's needs and requirements would be different. The consultation doesn’t seek to be too prescriptive, recognising this variation. However, legislation will be brought in to mandate that prior to assets being declared dormant as part of participation in the expanded scheme, proportionate and reasonable tracing efforts to reunite assets with their rightful owners need to be carried out.

The industry champion's seven-stage process

What’s next?

We welcome your thoughts and comments before we submit a response to the consultation, so please feel free to email us.