Employee Share Plans

Designing an employee share plan involves several financial reporting considerations. The impact to a company's Share Based Compensation Expense reporting and associated disclosures (i.e. IFRS 2, USGAAP, ASC718) is a vital consideration in designing an equity compensation plan. During the design phase, organisations need to assess the financial impact of recognising share-based payments in the profit and loss statement, ensuring regulatory compliance, while supporting broader business strategy. Common considerations include:

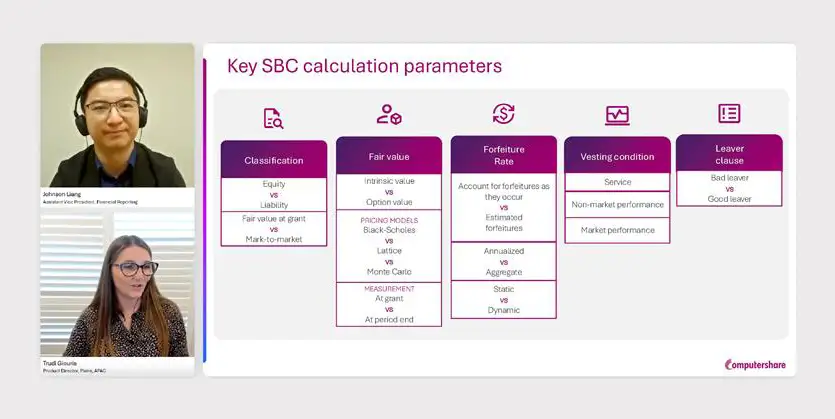

A company first needs to decide whether to grant restricted stock, stock options, or both at the initial plan design stage. The expense impact of the awards granted should be considered, alongside the complexities associated with Fair Value Measurements for share-based compensation. While RSUs valuation is generally simpler using the closing stock price as the Fair Value, stock options can be more complicated requiring option pricing models such as Black Scholes, Binomial method and Monte Carlo simulations.

Equity-settled awards are measured at their fair value on their grant date, with no subsequent changes to the value. Cash-settled awards require mark-to-market (MTM) at each reporting date until their settlement, typically resulting in additional workload on administration and reporting. Equity-settled awards have a relatively stable month-to-month expense, while cash-settled awards have a more fluctuating expense and impose financial burden on company's cash flow.

Share-based payments are typically subject to a vesting schedule. It's important to understand the three main types of vesting schedules:

Cliff vesting requires employees to complete a specific period before becoming fully vested or fully entitled to their benefits. Share-based compensation expense is amortized evenly over this period.

Graded vesting is a method in which vesting takes place in a gradual manner and employees are entitled to a bigger percentage over time. The straight-line attribution method and the accelerated attribution method can lead to different expensing processes throughout the vesting period.

While not common, immediate vesting does not require a grantee to provide any service to receive and be fully vested in RSUs or stock options. In this case, they are immediately expensed without any amortisation to follow.

Companies typically require employees to fulfil certain conditions to earn and retain stock-based compensation awards, as part of their retention strategy. An award is considered vested when an employee's right to receive or retain the award is no longer contingent on satisfying the vesting condition. In general, there are three types of vesting conditions:

Requires an employee to remain employed at the company for a predetermined period of time (i.e. time-based vesting).

As these are tied to company financial performance metrics such as Earnings Per Share (EPS), Total Shareholder Return (TSR), Relative TSR (a comparison against industry peers) and profitability metrics. These are generally favoured by shareholders.

Metrics are used to assess performance that are not directly tied to market value or share prices. These focus on operational, strategic, or qualitative measures, such as ESG targets, Customer Satisfaction, Brand Reputation, Risk Targets etc.

Where awards are subject to performance conditions, the accounting approach and valuation methodology differ (e.g., amortization method, expense recognition period, fair value measurement), from arrangements that vest solely over time. How expense is recognised and reported over time depends on whether the performance vesting conditions are based on non-market or market performance conditions. The key accounting difference is that market performance conditions are included in the grant-date fair value and not reassessed, while non-market performance conditions are excluded from initial valuation and require ongoing reassessment on their achievement results.

Companies can determine whether the employee will receive dividends paid on the underlying shares for the unvested RSUs. If the grantees of the RSUs are entitled to dividends, the expected dividends should be incorporated in the measurement of the grant date fair value of RSUs.

Determining whether the grantee is an employee or non-employee is an important part of the plan design, as this determines the accounting for the award. Generally, common law employees and directors that are elected by shareholders, and who receive awards for services as directors, are employees. A non-employee is considered an independent contractor, consultant, temporary worker, or vendor. Other factors to consider when determining employee vs non-employee include:

The cost of share-based payments can be recognised over the employee's requisite service period or the non-employee's vesting period.

Companies should elect to estimate forfeitures of employee awards based upon providing the requisite service. Consequently, an estimated forfeiture rate is adopted in share-based compensation for employees, while it's not required for non-employees.

Fair value measurements procedures on employee awards and non-employee awards may vary depending on the accounting standards that companies follow.

In summary, a company's share-based compensation financial reporting needs to be thoughtfully considered when designing an effective share plan. Key decisions such as choosing between RSUs and stock options, equity or cash settlement, and the structure of vesting directly affect accounting treatment, tax obligations, and employee retention. Companies need to balance between cost predictability, EPS dilution, and administrative complexity, while ensuring alignment with local market standards.

Partnering with an experienced service provider like Computershare is essential for smooth plan design, execution, and compliance with financial reporting requirements. Our expertise in global equity administration and deep knowledge of financial reporting requirements help minimise operational risks. Companies can stay focused on strategic priorities while ensuring their equity plans are both effective and compliant.

We have over 1,000 equity experts across all major markets, ready to help you design and deliver the right employee equity solutions.