Background

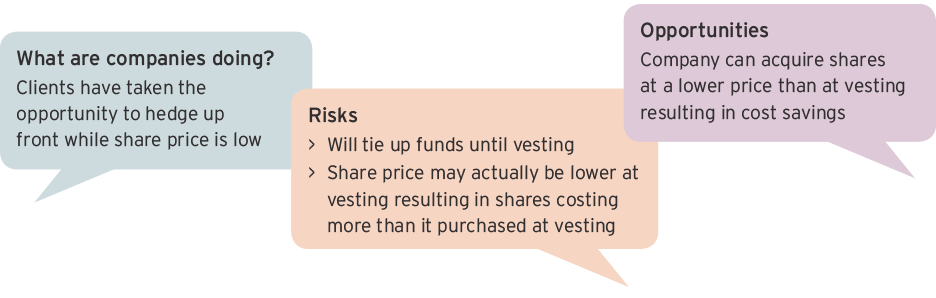

Download ArticleA company grants various award plans, including Restricted Share Unit (RSU) and Performance Share Unit (PSU) plans; the awards are structured to settle in three (3) years with shares acquired on the market at vesting. The company’s share price has decreased significantly and suddenly but is expected to increase again over time and is looking for ways to potentially minimize future share acquisition costs related to settling these awards.

Strategy

Where a company has a reasonable expectation that its share price will recover from a decline in stock price over the lifespan of the stock-settled RSU / PSU awards it’s granting, one way to minimize future share acquisition costs related to the settlement of the awards is to establish an Employee Benefit Plan (EBP) trusteed by a recognized trust company to facilitate the purchase of shares at grant (noting that the trustee does not need to be the plan administrative agent). This will crystalize the cost of the shares and protect the company against future share price increases. The trustee then holds the shares in the EBP trust until required to distribute the shares at redemption.

Considerations

The company must have enough funds available, which it can afford to lock up until the awards redeem. This mechanism also does not guarantee cost savings as the company’s share price will not necessarily be higher at award redemption. There are also detailed rules as to when the plan sponsor can expense the employer contributions for purposes of income tax; however, in general, the plan sponsor can expense the employer contributions only when the shares are distributed from the trust and at their original cost.

The participant also has taxable employment income only when the shares are distributed from the EBP trust (with taxes being withheld/collected by the trustee), based on the fair market value (FMV) of the shares on the vesting / distribution date (and not the original cost).

Additional Decisions

What will the company’s approach be to purchasing shares that are subsequently forfeited?

Best Practices

In our experience, clients typically purchase enough shares to bring the trust to a certain coverage percentage, being 100% or a lesser percentage factoring in estimated forfeitures. This approach factors in actual forfeitures on an ongoing basis which minimizes purchases to achieve the desired coverage percentage.

How will dividends that will not be paid out of the trust in the same year as received be handled? For example, where the company pays dividends and the dividends will not be paid out of the trust in the same year as received, the dividend income becomes taxable to the trust, resulting in the trust, to the extent the trust does not have offsetting expenses, being liable to pay taxes.

Some clients elect to have the dividends distributed from the trust back to the plan sponsor (client) as income to the plan sponsor, where such funds are either retained (typically where awards do not attract notional dividend equivalents) or contributed back to the trust as an employer contribution (typically where awards do attract notional dividend equivalents). Other clients, typically where awards do not attract notional dividend equivalents, have instructed the trustee to hold the shares as a registered shareholder with a dividend waiver in place.

Any company interested in considering an EBP is encouraged to speak with their legal and tax advisors to determine feasibility, applicable tax implications, timing and amending their plan texts. Computershare Trust Company of Canada can assist you in establishing an EBP trust, including providing a template EBP trust agreement. To learn more about all the services we can offer you, visit us at computershare.com/employeeshareplans.

No investment advice. This content is for general information and should not be relied up as, or construed as, investment advice, financial advice or other advice.

Learn More

Computershare (ASX: CPU) is a global market leader in transfer agency and share registration, employee equity plans, mortgage servicing, proxy solicitation and stakeholder communications. We also specialize in corporate trust, bankruptcy, class actions and a range of other diversified financial and governance services.

Computershare’s employee equity plans business offers full-service administration for plans of all types. With offices around the world, we support 1500+ clients with 5.3 million participants in 170 countries. We offer a single, global platform for both participants and administrators alike to manage their plans with ease, no matter where they are located.

For more information, please fill out the form below:

Due to Canada’s Anti-Spam Legislation, we are required to obtain your consent to send you commercial electronic messages. By selecting 'Yes' and submitting this form, you consent to receive electronic marketing messages from Computershare Canada and its affiliates about the topics noted above. You can withdraw your consent at any time by clicking on the unsubscribe button which is available in all electronic communications. To find out how we collect, use and safeguard your personal information, please refer to our

Privacy Code.

*Includes Computershare Canada Inc., Georgeson Shareholder Communications Canada Inc., Computershare Governance Services Ltd. and their majority owned subsidiaries operating in Canada (collectively referred to as "Computershare Canada").